Continued optimism despite inflation fears

Continued optimism despite inflation fears

08 Jul 2021

XPS Investment Monthly Update

Quarter in brief

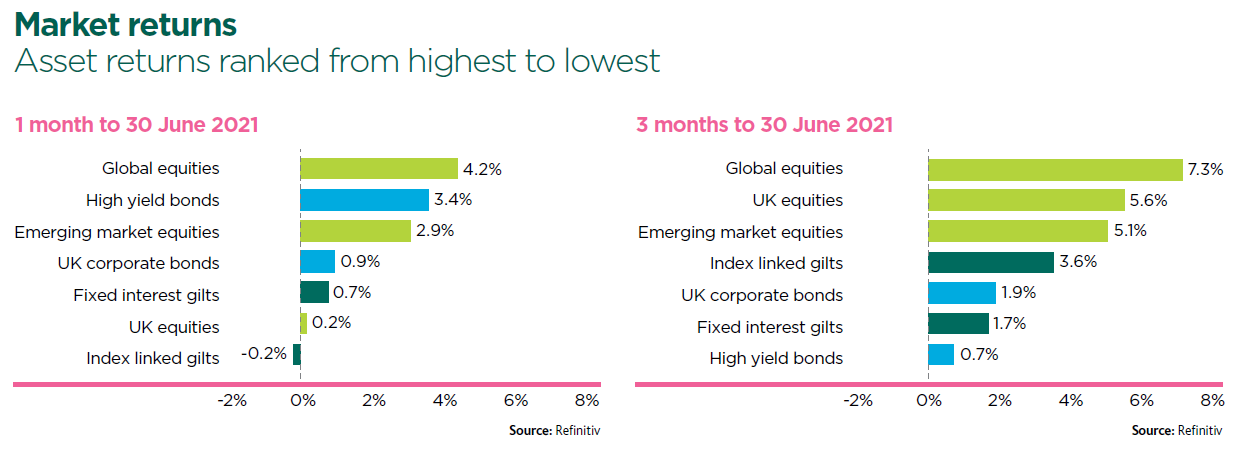

- Global equities produced positive returns as economic activity continues to recover.

- Gilt yields fell, reversing some of their significant gains over Q1 2021.

- Key worries for investors include inflationary pressures and the pace at which stimulus might be removed.

Major equity indexes closed out the quarter at or near record highs following a June rally powered by technology stocks. Falling gilt yields led to positive returns for bond investors.

Positive market sentiment continued to drive markets over Q2 2021. There was a raft of positive economic data including the Organisation of Economic Co-operation and Development (OECD) revising its economic growth forecast for 2021 up from 4.2% (December 2020 forecast) to 5.8% and positive Purchasing Managers’ Indices (PMIs). There was further evidence that the global recovery is uneven, with the OECD noting signs of more rapid recovery in the economies of those nations who dealt with Covid more effectively and who are further on with their vaccination programmes.

Equity markets managed to shrug off concerns over new Covid variants, particularly the emergence of the Delta variant. The global vaccine rollout continues with further evidence of vaccines’ effectiveness against the known variants of the Covid-19 virus. April and June saw strong gains but concerns over the prospect of increasing inflation, a tighter labour market and increasing input costs led to a sharp sell-off mid-May. The US Federal Reserve (Fed) sought to reassure investors that inflationary pressures were likely to be temporary, and that it would maintain its accommodative monetary policy stance. As a result, markets recovered to end May broadly flat.

While the Fed held rates stable following its June meeting, the big surprise was in the Fed’s signalling, through its now infamous ‘dots’ interest rate projections. These indicated an expected two rate hikes of 0.25% by the end of 2023, whereas previous guidance had been for no hikes until 2024. Also in the US, equity markets were supported by the Biden stimulus plan despite it having been watered down to achieve bipartisan support. US equity markets were not unduly impacted by Biden’s proposed tax increases or him committing the US to cut carbon emissions by 50%-52% by 2050 relative to 2005 levels.

Economists expect the UK economy to bounce back to its pre-COVID-19 level by the end of the year, despite the announced delay to the end of lockdown restrictions. The Confederation of British Industry has upgraded its latest forecast for the UK economy, predicting GDP growth of 8.2% this year, up from a previous forecast of 6%. June’s Purchasing Managers Indexes (PMIs), for both manufacturing and services, were above the 60 mark (50 indicating a stable outlook).

The headline unemployment rate fell for a fourth month to 4.7% in the three months to April, in line with expectations. The UK and Australia have reached a trade deal that will see a gradual wind-down of tariffs between the two countries and opens up new work visas for youngsters. However there was continuing post Brexit tension between the UK and EU in relation to Northern Ireland. UK equities returned 5.6%, underperforming global equities which returned 7.3%.

Consumer price inflation hit a two-year high of 2.1% in the year to May, above the Bank of England’s 2% target, with transport costs being the largest contributor. The Bank held monetary policy and interest rates unchanged in its June MPC announcement. It expects inflation to run above 3% in the near term as the UK economy reopens, but then ultimately settle closer to its target in the medium term. Longer term inflation expectations rose in late May but settled back down over June.

Fixed interest and index-linked gilt yields fell moderately over the quarter albeit following significant rises over Q1 2021. Sterling investment grade corporate bonds produced positive returns driven by falls in gilt yields with the spread (the additional return on corporate bonds compared with similar gilts) remaining stable at compressed levels, demonstrating low levels of perceived risk. Investment grade corporate bonds outperformed high yield corporate bonds predominantly due to the lesser impact of gilt yields on high yield bonds given their shorter maturity on average.

The funding level of a typical UK pension scheme improved over the quarter. Strong growth asset returns more than offset the impact of the higher value placed on liabilities as gilt yields fell.

"Consumer price inflation hit a two-year high of 2.1% in the year to May."

The typical scheme used has an assumed asset allocation of 24% equities, 33.8% corporate bonds, 12.6% multi-asset, 5% property and 24.6% in liability driven investment (LDI) with the LDI overlay providing a 60% hedge on inflation and interest rates. This example scheme was 80% funded in 2015.

To discuss any of the issues covered in this edition, please get in touch with Simeon Willis or Mark Searle, or your usual XPS contact.

- Register for events

- Join our mailing list

Register for events

We enjoy hosting a wide range of events for pension scheme trustees, corporate sponsors, independent trustees, and pensions professionals.

Join our mailing list

Keep up to date with our latest news and views including pension briefings, XPS insights, reports and event invitations.