Global equities erase all losses experienced in 2020

Global equities erase all losses experienced in 2020

07 Jul 2020

XPS Investment News

Bringing you our market round-up and the latest news affecting UK pension scheme investments.

In brief

- Equity and credit assets rallied strongly over the quarter as positive sentiment returned

- UK GDP contracted by 20% over April, but a V-shaped recovery is now being forecast by the Bank of England’s chief economist

- Funding levels improved over the quarter as asset performance outweighed an increase in liabilities

Key considerations for trustees

- How should a deteriorating covenant, negative gilt yields and a high level of government spending influence your strategy?

- Is there opportunity for your scheme to get a better match from your Liability Driven Investment strategy?

Q2 2020 saw equity and credit assets rally strongly to rebound from lows near the end of March. For a Sterling investor, global equities, UK corporate bonds and high yield bonds are now in positive territory for their performance over the first half of 2020.

During the quarter, most developed countries saw declining rates of new COVID-19 infections. The main exception to this was the US, where infection rates followed this trend to start with, but picked up materially in June. Markets have largely shrugged off the threat of a second wave and positive sentiment has returned, spurred by central bank and government stimulus that continues to be made available. The re-opening of economies and resumption of business activity has provided optimism among investors that economic activity may be rebounding quickly.

Equity markets seem content with other prominent threats, such as USChina tensions, China’s Hong Kong crackdown, the stuttering progress of EU-UK transition talks and the ripple effects that rising unemployment and corporate bankruptcies from the crisis are likely to have. Equities remained extremely volatile, frequently rising or falling by more than 2% over a 24 hour period.

Economic data has confirmed the stark reality of the impact that lockdown restrictions have had globally. More recently released data in June, whilst still relatively poor, exceeded market expectations. A good example of this is the UK economy where GDP contracted by 20% over April, but a V-shaped recovery is now being forecast by the Bank of England’s chief economist and GDP forecasts for the first half of the year have now been revised upwards from a 27% contraction to a 20% contraction. Meanwhile, job losses in the UK continue to increase materially.

Credit markets also recovered strongly over the period, with credit spreads tightening materially from highs near the end of March, with bond prices rising. This spread tightening has benefitted from many of the factors driving the positive sentiment in equity markets. In addition to this, market liquidity has improved significantly as a result of the large-scale monetary measures that have been introduced.

Official data published showed that the UK government’s debt exceeded the size of the UK economy in May for the first time in 50 years. The UK government is also now selling negative yielding debt up to 7 year maturity. Strong asset performance outweighed an increase in liability values over the quarter for a typical pension scheme, leading to an overall increase in the funding level of a typical scheme.

The typical scheme used has an assumed asset allocation of 24% equities, 33.8% corporate bonds, 12.6% multi-asset, 5% property and 24.6% in liability driven investment (LDI) with the LDI overlay providing a 60% hedge on inflation and interest rates. This example scheme was 80% funded in 2015.

We summarise our view on asset classes below:

XPS Investment Asset Class Views

Investing through the crisis... your questions answered

Question 1:

How and when should Trustees tackle specific risks within their investment portfolios and especially in terms of a weakening sponsor covenant?

For many schemes, the potential for the covenant to change in the future is the main driver for pursuing a path to a low dependency level of funding. Where this starts to get complicated is when this objective translates to taking higher returns to get there. A balance has to be struck, making sure the long term target is sufficiently low risk to meet your objectives, whilst ensuring the path to get there is also within your risk tolerance. This balance is at the heart of a well-structured journey plan.

Once this journey plan is in place it is important to revisit it in light of changes. COVID-19 provides a stark reminder that covenants can change in unexpected ways. In addition to reassessing your covenant you will need to know the impact that the crisis has had on your funding position, and then look at what the current strategy means for the prospect of meeting your objectives and the downside risk going forwards. With this essential information you can assess whether it is appropriate to reduce, maintain or even increase risk. This decision will be unique to every scheme.

In terms of timing, that part is easier to answer – there’s no time like the present.

Question 2:

How can Trustees have a gilts based journey plan assumption when they are likely to have a negative yield?

There are a variety of approaches that can be taken in relation to valuations and journey planning. A gilts based approach is very popular given that it is well understood and there are established means to manage a scheme’s risk and investment strategy alongside it. The negative nominal gilt yields we have seen recently do not undermine the merits of a gilts based approach. After all, we have been used to working with negative real gilt yields for some years now and nominal yields are not that different.

What can be difficult to reconcile is that negative interest rates and nominal yields implicitly mean that holding cash in the form of notes and coins (known as M0) generates a higher relative return than investing in deposits and short term money market instruments. Put another way, earning nothing is better than making a loss. However, in practical terms it is not possible to do this with large sums of money due to storage, logistics and security issues. Who is going to keep your £1m worth of £50 notes safe? As such, generating out performance from holding M0 is not an option for institutional investors.

Whilst the concept of paying a government to borrow your money may feel uncomfortable, the impact it has on schemes and journey plans is relatively straight forward. As the yield falls into negative territory the impact on the liability value behaves in the same way as it would do normally if there is a fall – the liability value increases slightly. There is no cliff edge or point where the whole approach disintegrates. Importantly, alternative approaches that don’t link to gilt yields still need to be monitored to check that the implicit return expectation doesn’t become unrealistic in the context of the lower returning environment we find ourselves in.

Question 3:

The new fiscal stimulus could possibly lead to a vast over supply in sovereign debt issuance. What are the implications for bond prices and yields?

In isolation, an increased supply of sovereign debt issuance should lead to an increase in the yields of sovereign debt, in order to generate the necessary buy-side demand to clear the market. This would be good news for pension schemes who are not fully hedged.

However, as with all economic policies it is important to consider the interaction with other dynamics in order to appreciate the possible implications for prices. Household savings rates have increased as part of the recessionary impact and demand for sovereign debt has remained strong as investors look for low risk investments. This, combined with expanded quantitative easing by the Bank of England and the potential for negative short term interest rates, is likely to lead to continued downward pressure on UK government bond yields. Further, it’s also worth remembering that monetary and fiscal stimulus are inflationary policies which could erode the real return that is earned on a fixed income asset.

At XPS we generally encourage our clients to look to hedge as far as is practical within their strategy, noting that their return target, diversification and liquidity all play into how much hedging can be practically achieved.

"The negative nominal gilt yields we have seen recently do not undermine the merits of a gilts based approach."

LDI – finding your perfect match

LDI has long since come of age in the UK market and now a primary focus for many Defined Benefit pension schemes is thinking about how and when they will get to being fully hedged on their interest rate and inflation risk.

In this short note we highlight some of the new challenges that a scheme will need to navigate when hedging more than 80% of their liabilities.

The first half of 2020 has been a savage reminder of the risks that pension schemes are exposed to. Well hedged schemes have been better protected against this environment and some of these schemes may even now find themselves better funded than at the start of 2020, following the rebound in equity and credit markets.

Obtaining high levels of hedging can present some new challenges. As the big picture risks are removed, smaller more stubborn risks will start working their way up the risk management agenda and this calls for greater precision in the Liability Driven Investment hedge design.

There are many complexities that need to be considered here. We have chosen a small selection of key issues that, in our experience, are often overlooked. We would note that controlling for many of these issues does not necessarily involve greater cost of implementation.

1. Cashflow mismatch risk

Usually when we talk of a scheme’s hedging ratio we are referring to the overall interest rate and inflation exposure of its assets compared to its liabilities. This overall measure is the first order of hedging, and the residual risk usually accounts for less than 10% of the original unhedged risk.

Importantly though, when you are approaching being fully hedged this residual risk will represent the vast majority of the remaining interest rate risk.

Using gilts inherently involves some cashflow mismatch. The extent of this depends on what combination of gilts you hold – illustrated in charts 1 and 2 – where the second shows a more balanced approach. Swaps offer a more precise means of hedging but for the last decade gilts have represented the cheapest hedging asset offering the highest yield. This has justified incurring some cashflow mismatch to reduce cost. However, it is still beneficial for the level of cashflow mismatch to be reduced as far as is practical whilst using the cheapest hedging instrument, so balanced hedges are preferable to long dated hedges.

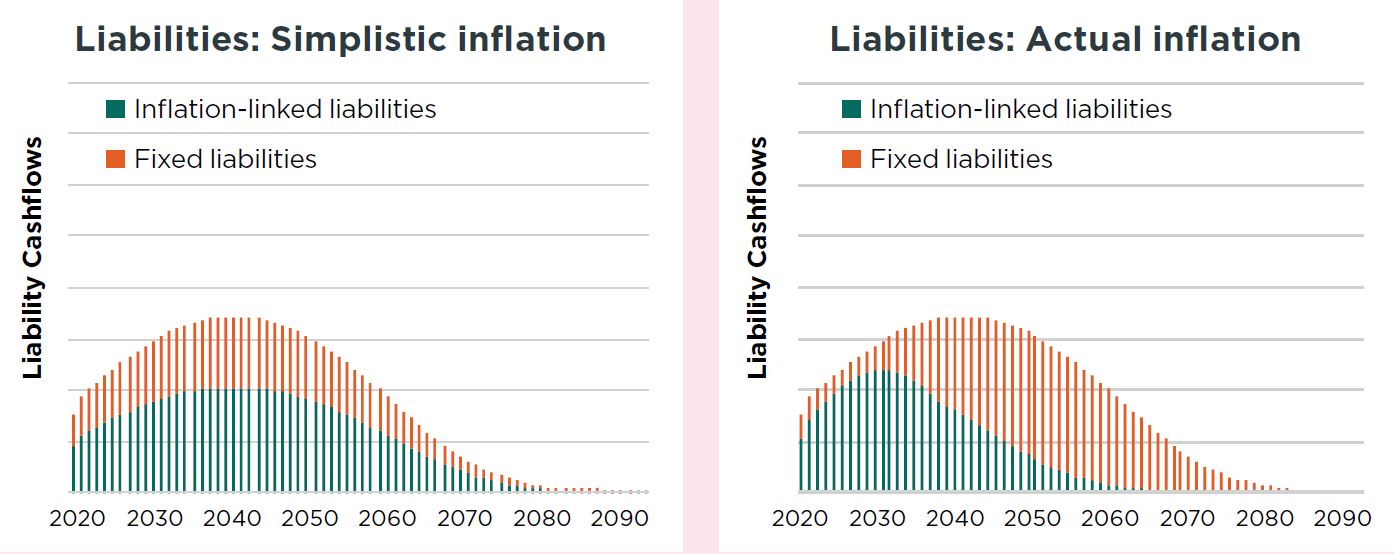

2. Inflation increases for members before and after retirement

One of the areas that directly impacts the fit of an LDI strategy is the difference in the way that pension benefits are increased each year for members before and after retirement.

UK DB liabilities typically offer more inflation linked increases for the phase before retirement than after retirement.

LDI mandates commonly approximate that the inflation exposure is evenly applied across the scheme’s projected cashflow profile, however the true exposure can be somewhat different. This is illustrated below.

The consequence is that schemes commonly buy too much long dated inflation protection and not enough short dated protection.

This can be addressed at the design phase by using granular “3D cashflows” when setting the benchmark for your LDI manager. 3D cashflows break out all the different types of pension increase so the LDI hedge benchmark can correctly reflect the underlying inflation risk. The additional information is akin to the extra dimension you have when looking at a 3D object rather than a 2D photo. You need that extra dimension in order to match your scheme’s exposure from different angles.

3. Inflation caps and floors

Inflation-linked benefits are often subject to a minimum level of increase of 0%pa and some sort of maximum, say at 3%pa, 5%pa or a variety of other limits. This is challenging because there are relatively few assets, if any, in the market that offer inflation that mirrors these caps and floors.

For pensioners, annual increases are typically capped each year. For deferred members, benefit increases typically look at the average inflation experienced over the whole period up to retirement for each member and then apply the caps and floors to this average rate.

This presents more challenges as the nature of the inflation is highly complex and unique to when a member retires and therefore is not possible to hedge with complete precision.

Hedging techniques can go a long way in terms of mirroring the broad characteristics required, but this requires careful analysis and regular updates to your fund manager’s hedge benchmark, to avoid the benchmark going stale. We recommend at least every 3 years, and more frequently if inflation expectations change significantly. Even so, some residual risk will still exist which needs to be recognised so that it does not take you by surprise.

4. CPI linked liabilities

Where a scheme has CPI linked benefits it is, in the most part, not practical to hedge these using assets that are liked to CPI. The market for CPI linked assets is small, illiquid and sought after, so it currently offers relatively limited application for most pension schemes.

Therefore, in the main, if you wish to hedge CPI liabilities it is necessary to approximate this with RPI linked assets such as Index Linked Gilts and RPI Swaps. The potential mismatch between RPI and CPI is currently exacerbated by the consultation on RPI reform. However the alternative is to run the naked inflation risk, a prospect which in the main is not very appealing.

Summary

We have established that there are a number of detailed issues that mean that a 100% interest rate and inflation hedge doesn’t mean 0% risk.

However, this should not lead to the conclusion that a 100% hedge should not be considered a desirable hedge target, quite the opposite. It just means that as you increase hedging there is merit in ensuring that you are getting the best possible match, particularly given that getting the right hedging structure needn’t cost more to implement. There will still remain some risk though, which cannot be avoided.

At XPS we have a comprehensive range of tools to help our clients achieve the best possible fit for their circumstances. Getting the right fit will significantly reduce risk and help you understand the remaining risks that you are exposed to, avoiding nasty surprises.

To discuss any of the issues covered in this edition, please get in touch with Simeon Willis. Alternatively, please speak to your usual XPS Investment contact.

- Register for events

- Join our mailing list

Register for events

We enjoy hosting a wide range of events for pension scheme trustees, corporate sponsors, independent trustees, and pensions professionals.

Join our mailing list

Keep up to date with our latest news and views including pension briefings, XPS insights, reports and event invitations.