The most challenging global economic environment in almost a century

The most challenging global economic environment in almost a century

06 Apr 2020

XPS Investment News - April 2020

Bringing you our market round-up and the latest news affecting UK pension scheme investments.

In brief

- In our February update, we observed that March would be a critical month in terms of the extent to which Coronavirus took hold globally

- With hindsight this was an understatement. What has since happened has shocked the world

- In this special report we look at quarter 1 2020, with a week by week focus on how markets reacted in March

Key considerations for trustees

- This may only be the start and there still remains a huge degree of uncertainty

- We project a range of forward-looking scenarios and how these could impact a typical scheme

- We conclude with key actions to help trustees plan for the future

Quarter 1 2020 will go down in history as one of the most volatile and eventful quarters that markets have ever experienced. Over January, and most of February, markets were focused on issues such as Brexit, trade wars, a potential slowdown in global growth and an escalation in tensions between the US and Iran. However, these events paled into insignificance compared to the impact that the spread of Coronavirus has had on global markets since the last week of February, where the virus went from being an ‘Asia problem’ to a global one.

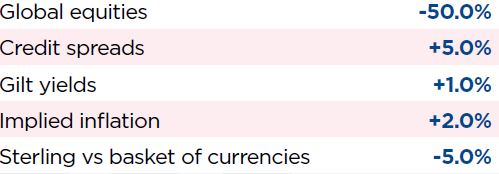

The spread of the virus outside of China has led to a partial economic shutdown for many countries. Equity markets went from being at, or close to, record highs for the majority of February, to experiencing their sharpest fall since 1987, and credit spreads have broadly doubled, reflecting the impact that the virus has had and will continue to have on the earnings of businesses and the wider asset markets. Central Banks and governments have reacted to the economic shock through the implementation of large monetary and fiscal measures, in order to defend their respective economies and soften the blow that this shock is going to have, as far as is feasible. UK government bond yields experienced wild movements in both directions, initially falling, reflecting their ‘safe haven’ status, then whipsawing temporarily as market liquidity dried up.

The typical scheme used has an assumed asset allocation of 27% equities, 34% corporate bonds, 11.6% multi-asset, 4.8% property and 22.6% in liability driven investment (LDI) with the LDI overlay providing a 50% hedge on inflation and interest rates. This example scheme was 80% funded in 2015.

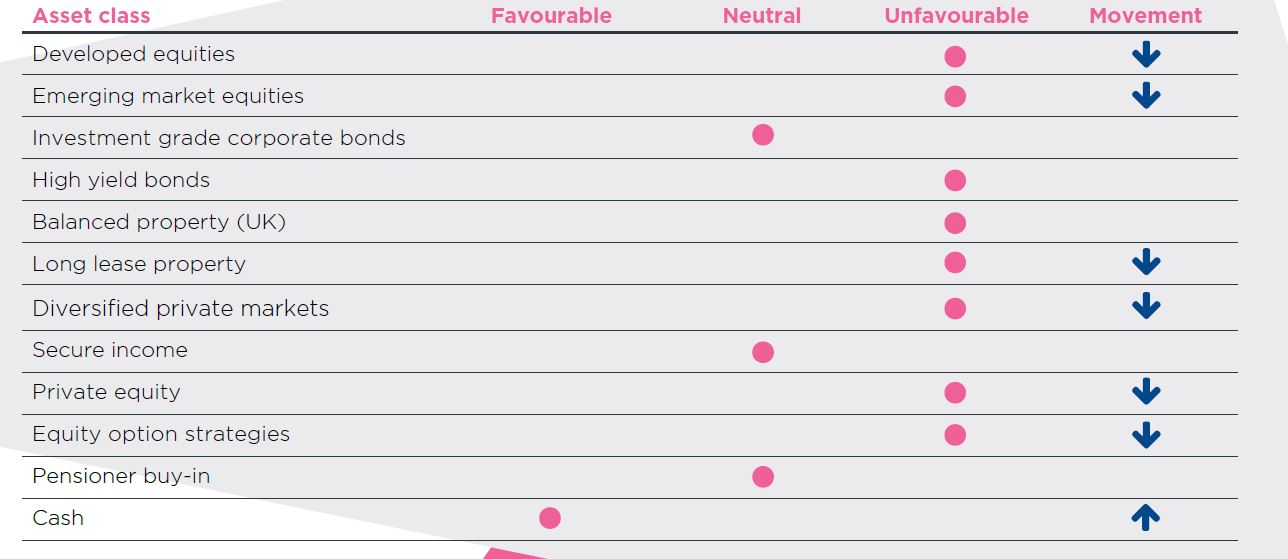

We summarise our view on asset classes below:

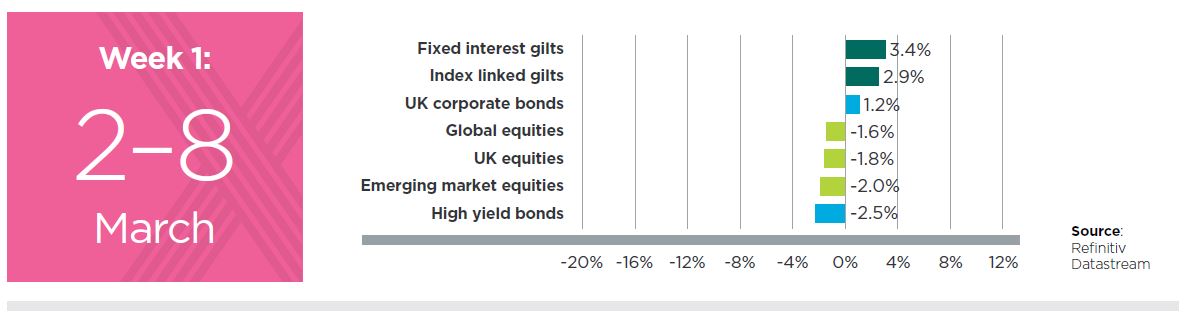

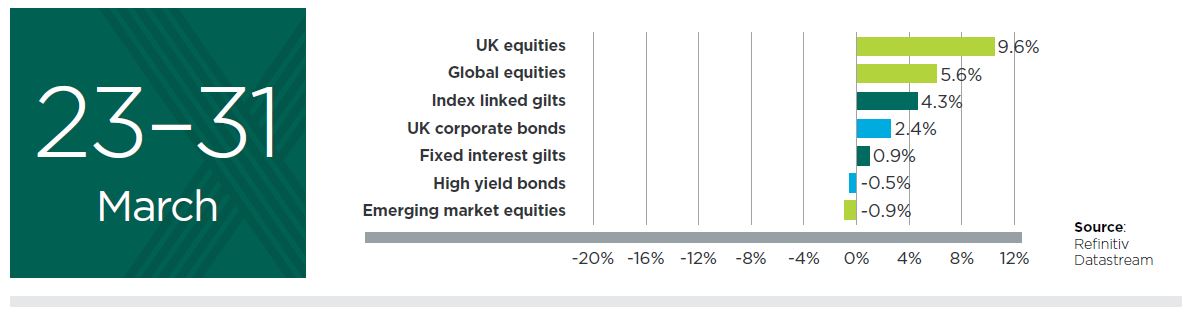

In focus - March Market Mayhem

- Global death toll reaches 3,827.*

- Fears around the increased spread and impact of the virus among Western countries resulted in a week of losses for risk assets.

- Investors rushed to the perceived safety of ‘safe haven’ assets which, alongside the expectation of more accommodative central bank policy, resulted in the yields of government bonds globally falling to record lows.

- The central banks of China, France, Italy, Japan and the US, to name a few, undertook various fiscal and monetary measures over the week to try and cushion the economic shock that the virus is expected to cause. In particular, the US Federal Reserve cut rates by 0.5% to 1-1.25%.

- This monetary stimulus failed to stop equity markets from posting negative returns over the week, as markets deemed that this alone was insufficient.

- Figures released by China showed that exports contracted by 17.2% in January and February, and Chinese manufacturing activity plunged to a record low over February. However, its stock market remained resilient.

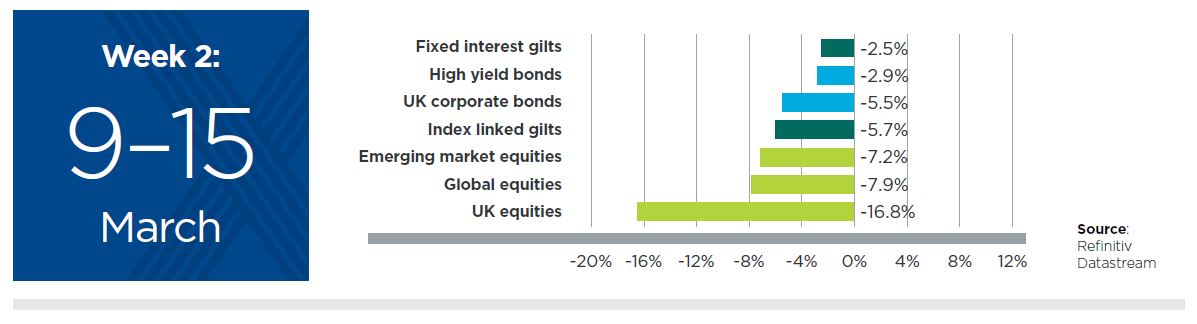

- Global death toll reaches 6,520.*

- Italy put its entire country in lockdown, and Spain closely followed, as Europe became the epicentre of the outbreak.

- Equity markets suffered huge loses and daily movements over the week.

- With markets already on edge, Saudi Arabia’s decision to start an all-out price war with Russia kick started the rout, with energy stocks, financials and other specific sectors particularly badly hit. Oil prices also fell materially.

- European countries continued to announce significant fiscal and monetary policies designed to reassure business and steady markets.

- The Bank of England cut interest rates by 0.5% to 0.25% and offered other monetary stimulus. The British government announced its first fiscal package as part of the Budget, which included £12bn of emergency fiscal stimulus.

- Stress began to appear in the US Treasury market as liquidity dried up and strange patterns emerged. In particular, the price of Treasuries fell at the same time that risky assets prices were falling. This was caused by the retreat of buyers and an increase of sellers, as investors looked to raise cash in any way possible.

- The US Federal Reserve sought to shore up liquidity by unveiling a multitrillion dollar operation to soothe the anxiety, amongst other new monetary measures. It also dropped its policy rate again, this time by a full percentage point to 0-0.25%.

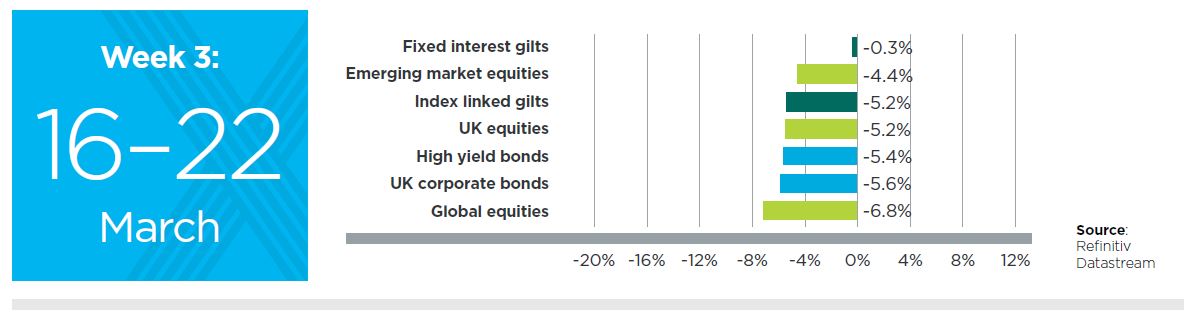

- Global death toll reaches 14,640.*

- Measures to tackle the virus were stepped up another level across Europe, as the UK entered a period of partial lockdown.

- The UK Government also announced unprecedented levels of fiscal stimulus, in the form of a £330bn package of emergency loans to businesses and £20bn of further fiscal support.

- The European Central Bank announced its plan to buy €750bn in bonds.

- The week saw further upward pressure on global government bond yields, which moved materially higher and spiked mid-week.

- Equities suffered another material fall. Credit spreads had been widening since the last week of February, and this continued, as they moved substantially wider over the week. This reflected an expectation of material losses to companies’ future earnings.

- Sterling weakened against other major currencies, and significantly against the surging US dollar (to its lowest level since 1985), offsetting some of the losses sterling investors would have experienced on global equity holdings.

- Figures released by China showed that over the first two months of the year; industrial output fell 13.5%, retail sales fell 20.5% year on year; fixed asset investment fell 24.5% and the urban unemployment rate surged to 6.2% in February.

- A wave of UK property funds gated in response to the inability of independent valuers to provide accurate and reliable valuations on the underlying properties.

- Global death toll reaches 42,309.*

- The number of infections and deaths within the US and Europe escalated significantly. China’s rate of new cases declined and the economy began to re-open as some restrictions were lifted.

- At the beginning of the period, equity markets touched their lowest close since the crisis began, but rebounded to make material gains as investors took comfort from the level of central bank stimulus implemented.

- In particular, investors reacted positively to the US Senate passing a $2trn fiscal support package and the Federal Reserve announced unlimited quantitative easing.

- Credit spreads narrowed over the week, although ended March significantly elevated.

- Data showed the extent of job losses suffered. In particular, nearly 3.3m Americans claimed jobless benefits, which was 4 times more than the historic record.

- For both the UK and the Eurozone, their respective HIS Markit flash Purchasing Managers Index, a survey of the manufacturing and services sectors, showed their lowest level ever, implying a sharp contraction in both economies.

- Sterling rebounded against the US dollar and euro.

- China’s official manufacturing index rebounded in March, coming in well above forecasts.

* source: worldometer.info

Looking ahead

Scenario analysis – 5 different paths

We have put together a range of forward-looking scenarios to identify how a typical pension scheme might be impacted by the various scenarios that could play out over the 6-12 months from the 31 March 2020. The scenarios considered are all coronavirus related, in line with our belief that the way that this crisis plays out will be the predominant driver of markets over the short-to-medium term.

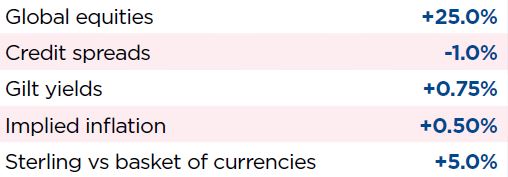

1) Minimal disruption

Funding impact on typical scheme: +12%

A transition towards normality is lead by China with a successful re-ignition of their economy and only isolated areas of re-infection. Immunity stands the test of time and western nations follow China in terms of returning to normal trading. Heavy central bank and government stimulus leads to a rally on the stock market with a pick up in inflation.

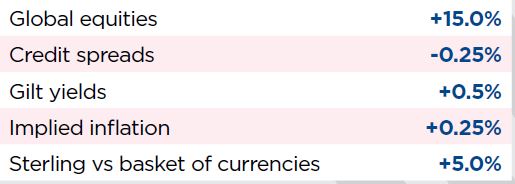

2) Better than expected case

Funding impact on typical scheme: +5%

Warmer weather suppresses infections and social distancing proves even more successful in the US than in other countries. Companies return to normal within 3 months and the positive government and banking stimulus provides a welcome boost, helping the economy to get back to work.

3) Central case

Funding impact on typical scheme: -5%

China gradually loosens grip on the lockdown and a moderate level of re-infection requires patience. The US and Europe get worse before they get better and a number of high profile bankruptcies shake the market. Life returns towards normality over a 6 month time period leaving a dent in GDP growth and substantial levels of unemployment.

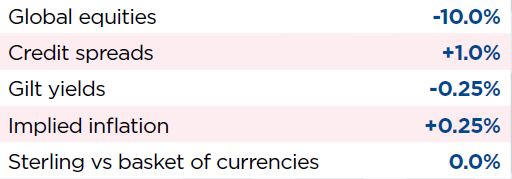

4) Worse than hoped

Funding impact on typical scheme: -14%

The US and Europe continue to struggle to contain the rising infection rates and the length of lockdown shifts beyond 6 months. Bankruptcies soar and further measures are taken to protect the public at prohibitive cost to governments. Monetary policy reaches its limit. Inflation expectations fall due to reduced demand.

5) Leads to a global depression

Funding impact on typical scheme: -26%

The measures taken to contain the virus outbreak lead to a global depression in addition to lost output for half of the year. The demand and supply shock combined with stimulus measures result in inflation and widespread insolvencies on a level not seen for almost a century. Government yields start rising to reflect default risk and a stagflationary environment develops.

Actions that pension schemes can take

In light of the current uncertainty, XPS has put together a key checklist for pension scheme trustees.

This should help ensure that a scheme is undertaking all necessary actions in response of market volatility to date, and is suitably positioned for any future market volatility that may occur:

- Review investment risk tolerances in current climate – especially what the employer is comfortable supporting in light of a possible deterioration in covenant

- Review portfolio liquidity and short term cash flow requirements

- Check your interest rate and inflation hedging has performed in line with expectations and consider increasing or refining the hedge to provide further protection

- Assess your underlying sector and regional exposure to understand if any undesirable concentrations exist

- If in the process of implementing a change to your strategy, reassess if it continues to be suitable in light of developments

- Consider holding a greater cash buffer to meet benefit payments, but avoid using the trustee bank account for this purpose (due to the unsecured risk of the bank)

To discuss any of the issues covered in this edition, please get in touch with Simeon Willis or Ben Gold

- Register for events

- Join our mailing list

Register for events

We enjoy hosting a wide range of events for pension scheme trustees, corporate sponsors, independent trustees, and pensions professionals.

Join our mailing list

Keep up to date with our latest news and views including pension briefings, XPS insights, reports and event invitations.