New COVID-19 variant,‘Omicron’, leads to sharp equity market pull-back

New COVID-19 variant,‘Omicron’, leads to sharp equity market pull-back

03 Dec 2021

Month in brief

- Global equities experienced their largest daily fall in over a year and credit spreads widened after discovery of new COVID-19 variant, Omicron

- Supply-side problems, alongside continued strong consumer demand, drive inflation higher

- Flash PMI numbers indicate slight deceleration in global growth, albeit growth remains above trend rates

Risk markets pulled back sharply over the last week of November after the discovery of ‘Omicron’, a new COVID-19 variant which has alarmed health officials and raised concerns globally.

The uncertainty surrounding the severity of the strain led to a material sell-off in risk markets, given the potential for widespread restrictions to be re-imposed in the event that vaccines are less effective against it.

Global equities experienced their largest daily fall in over a year as a result and credit spreads widened, reflecting an increased risk of default. Conversely, government bond yields fell globally as investors moved into ‘safe-haven’ assets.

Up until that point in the month, equity and credit market performance had generally been strong. Employment data for the UK and US surprised on the upside, particularly in the UK where employment rose in the month after the closure of the government’s furlough scheme, which was still supporting more than a million jobs in September. Flash Purchasing Managers Index surveys for November indicated that the world’s largest developed economies continue to grow at above trend rates in the fourth quarter, albeit activity levels have decelerated slightly relative to the levels of activity seen in Q3.

However, global supply-side issues, including rising energy prices, supply chain issues and labour shortages, combined with strong consumer demand, pushed inflation higher. UK and US annual CPI inflation hit 3.8% and 6.2%, respectively, in October. This is putting pressure on central banks to raise rates, which could combine with Omicron to dampen economic growth. The US Federal Reserve has responded to this inflation risk and buoyant US economic activity by announcing plans to wind back its $120bn a month stimulus programme.

Eurozone inflation increased to 4.9% in November, which is the highest level since the creation of the single currency. In contrast with the US and UK, the European Central Bank has so far pushed back against suggestions that it should reduce current levels of monetary stimulus to try and control inflation, pointing to what they see as temporary one-off causes. A surge in COVID-19 cases in Europe led to certain countries, including Austria, Ireland, Germany and more, to re-introduce related restrictions.

The material rises in energy prices have created significant headwinds for UK energy suppliers, particularly those with inadequate hedging policies in place. Over the month, Bulb, Britain’s seventh biggest supplier became the 23rd energy supplier to collapse in the UK since the beginning of August.

UK gilt yields remained volatile throughout the month due to inflation concerns. Credits spreads widened at the end of the month, detracting from credit returns, however the high yield return shown is a global index and outperformed UK corporate bonds as a result of sterling depreciation over the month.

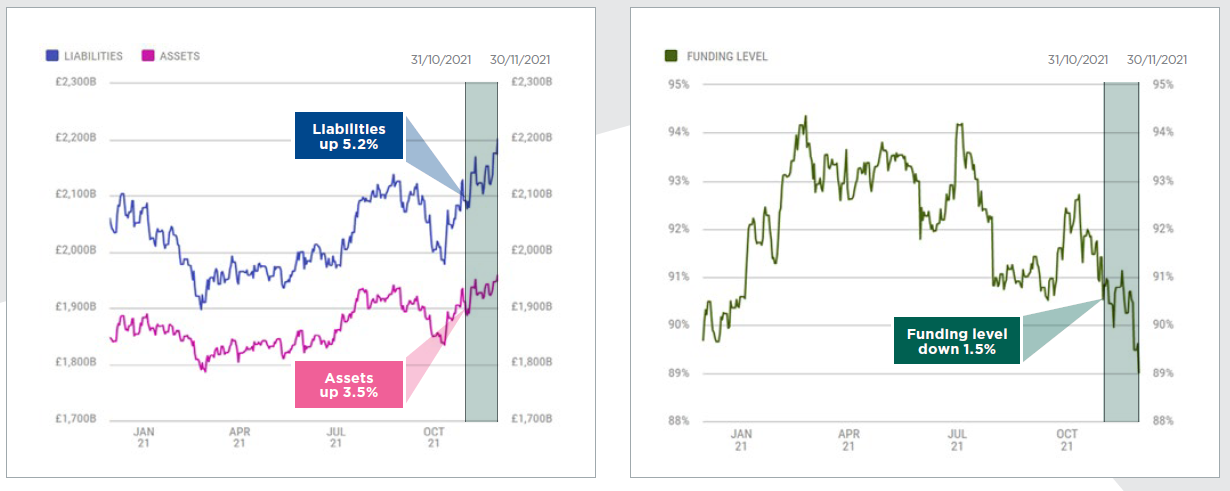

The estimated aggregate funding position of UK DB pension schemes fell over November, owing to an increase in liability values driven by falls in gilt yields and increasing inflation expectations outweighing positive asset performance.

Source: XPS DB:UK

The charts above are based on data from The Pensions Regulator, the PPF 7800 Index and the XPS data pool. The assumptions used in the UK:DB long-term target basis include a discount interest rate of gilt yields plus 0.5%. The assumed asset allocation is 16.9% equities, 20.0% corporate bonds, 6.9% multi-asset, 5.1% property, 3.8% private markets and 47.3% in liability driven investment (LDI) with the LDI overlay providing a 60% hedge on inflation and interest rates.

For further information, please get in touch with Sian Pringle.

- Register for events

- Join our mailing list

Register for events

We enjoy hosting a wide range of events for pension scheme trustees, corporate sponsors, independent trustees, and pensions professionals.

Join our mailing list

Keep up to date with our latest news and views including pension briefings, XPS insights, reports and event invitations.